Investor Alert:

CIRO is warning Canadian investors about fraudulent emails impersonating Interactive Brokers Canada Inc. (IBKR), a CIRO member.

Effective Date: December 31, 2024

This Guidance Note is being issued to provide:

Dealer Members play an important role in issuer company capital raising by agreeing to:

Where a new issue involves Dealer Members assuming an underwriting liability, distinct activities are agreed to and carried out by the:

The carrying out of these activities is important to ensuring that the new issue offering is widely and fairly distributed to investors wanting to participate in it and the issuer company raises its capital in a cost-efficient manner.

Guidance on regulatory financial reporting and capital requirement issues that arise when a Dealer Member assumes a new issue underwriting liability

Where a Dealer Member assumes a new issue underwriting liability (as a syndicate group member), both regulatory financial reporting and capital requirement issues arise due to their assumption of new issue underwriting risk.

The regulatory financial reporting issues that arise largely relate to determining when an underwriting commitment has been entered into and when new issue sales can be recorded. The capital requirement issues that arise almost exclusively relate to determining how to provide for the residual new issue underwriting risk during and after the offering distribution period.

The remainder of this Guidance Note provides guidance on these issues by responding to commonly asked regulatory financial reporting and capital requirement questions relevant to when a Dealer Member assumes a new issue underwriting liability. These questions and the pages within this Guidance Note where these questions are discussed are as follows:

Several forms of financing agreements are currently in use within Canada. In some cases, the financing agreement terms do not make it clear whether the Dealer Member is entering into an agency financing or an underwriting commitment. Whether or not entering into a financing agreement constitutes a committed underwriting is a question of fact. If enough pricing terms (in addition to all other non-pricing terms) are agreed to, the Dealer Member has entered into an underwriting commitment.

A Dealer Member is only required to report financial information within Investment Dealer and Partially Consolidated (IDPC) Form 1 when it has entered into an underwriting commitment. To assist in determining whether a Dealer Member has entered into an equity security underwriting commitment, a definition of the term “commitment” is set out in IDPC Rule subsection 5130(5). The definition stipulates that two of the following three pricing terms (in addition to all other non-pricing terms) must be agreed to before a Dealer Member is considered to have entered into an equity security underwriting commitment:

Since the equity security issue commitment amount is equivalent to the issue price multiplied by the number of shares, agreeing to any two of the above three terms will effectively means the third term has been agreed to as well.

A similar approach would be applied in determining whether a Dealer Member has entered into a fixed income security underwriting commitment. Specifically, where any two of the following three pricing terms (in addition to all other non-pricing terms) are agreed to by a Dealer Member:

and the issue commitment amount is also agreed to, the Dealer Member is considered to have entered into a fixed income security underwriting commitment.

Under an agency financing agreement, the Dealer Member does not commit to purchase a specified number of shares at a specified issue price (or in the case of a fixed income offering a specified issue commitment amount, at a specified price and coupon rate) but rather agrees to market the securities offering for the issuer, as agent, on a best-efforts basis. As a result, agency financings are not considered to be committed underwritings.

Once it has been determined that a Dealer Member has entered into an underwriting commitment, for all or a portion of a particular securities offering, the Dealer Member must record both its obligation to the issuer as a liability and the offering securities position it has agreed to buy as an asset. The Dealer Member’s share of the obligation to the issuer must be recorded, based on the agreed upon offering issue price. The amount of the obligation initially recorded cannot be reduced by deducting any underwriting fees it is to receive pursuant to the underwriting agreement. The offered securities position should be recorded based on its market value, which initially will be the same as the commitment obligation.

Where a Dealer Member has entered into an underwriting commitment it must:

During the period from underwriting commitment date to underwriting settlement date, the Dealer Member assumes the risk that it will not be able to sell all of its portion of the underwriting commitment by the underwriting settlement date. To address this risk, the Dealer Member must either:

Acceptable hedges that can either reduce or eliminate the capital required on the unsold portion of the Dealer Member’s underwriting commitment include:

The required minimum terms that must be included within any SFNIL that a Dealer Member enters into are that:

the loan issuer must:

to ensure that the loan issuer can advance adequate funds on settlement date

the loan issuer must agree to advance funds on settlement date:

and

A sample SFNIL template is available on the CIRO website.

The required minimum terms that must be included within any capital rental arrangement that a Dealer Member enters into include the following minimum terms:

Common approaches that can be used by the Dealer Member to meet its funding obligation to the issuer on the underwriting commitment settlement date include:

In the case of the subordinated loan option, there is no mandatory minimum term for the loan agreement, but the loan may not be repaid without the approval of CIRO.

Generally, to comply with generally accepted accounting principles, all security positions held must be marked to market daily. However, in the case of unsold underwriting positions the following should be considered:

As a result, the value reported for any unsold portion of an underwritten position during the period from underwriting commitment date to underwriting settlement date should be determined as follows:

For example, consider a situation in which a Dealer Member has agreed to the following underwriting commitment.

| Situation (a) – Market value $21.50 per share |

| Where the market value of the underwriting is $20 per share or greater, the unsold portion of the underwriting shall be valued at $20 per share. |

| Result (a) – Reported value of unsold portion is $20 per share |

| Situation (b) – Market value $19.50 per share |

While the result is the same as in Situation (a), the rationale is different. Specifically, it doesn’t make sense to write-down unless the market value is less than the net issue value of the unsold portion of the underwriting. In this example, the net new issue price per share is: = new issue price per share – underwriting fee per share = $20.00 – 5% x $20.00 = $19.00 As a result, where the market value of the underwriting is $19 per share or greater and less than $20 per share, the unsold portion of the underwriting shall be valued at $20 per share. |

| Result (b) – Reported value of unsold portion is $20 per share |

| Situation (c) – Market value $17.50 per share |

Where the market value of the underwriting is less than $19 per share, the unsold portion of the underwriting shall be written down by the amount of this drop in value below net issue price. In this example the drop in value below the net new issue price per share is: = net new issue price per share – market value per share = $19.00 - $17.50 = $1.50 As a result, the unsold portion of the underwriting shall be written down from the new issue price by $1.50 per share and therefore valued at $18.50 per share. |

| Result (c) – Reported value of unsold portion is $18.50 per share |

| IDPC Rule reference | Effective margin rates that apply based on issue market value per share | ||||||

|---|---|---|---|---|---|---|---|

| Category of security or security market value per share | Included on LSERM | >= $2.00 | >= $1.75 and <= $1.99 | >= $1.50 and <= $1.74 | < $1.50 | ||

| Capital requirements for equity security prospectus offerings in distribution are: | |||||||

| Without documented expressions of interest from exempt purchasers | Margin rate with no SFNIL or out clauses in effect | 5520(2) | 15.00% | 40.00% | 60.00% | 80.00% | 100.00% |

| Margin rate with no SFNIL but with disaster out clause in effect | 5520(3) | 7.50% | 20.00% | 30.00% | 40.00% | 50.00% | |

| With documented expressions of interest from exempt purchasers | Margin rate with no SFNIL or out clauses in effect | 5522(2) | 3.00% | 8.00% | 12.00% | 16.00% | 20.00% |

| Margin rate with no SFNIL but with disaster out clause in effect | 5522(3) | 3.00% | 8.00% | 12.00% | 16.00% | 20.00% | |

| With or without documented expressions of interest from exempt purchasers8 | Margin rate with no SFNIL but with market out clause in effect9 | 5520(4), 5520(5), 5522(4) and 5522(5) | 1.50% | 4.00% | 6.00% | 8.00% | 10.00% |

| Margin rate with SFNIL in effect but no out clauses in effect | 5521(2) and 5522(6) | 1.50% | 4.00% | 6.00% | 8.00% | 10.00% | |

| Margin rate with SFNIL and disaster out clause in effect | 5521(3) and 5522(6) | 1.50% | 4.00% | 6.00% | 8.00% | 10.00% | |

| Margin rate with SFNIL and market out clause in effect | 5521(4), 5521(5) and 5522(6) | 0.75% | 2.00% | 3.00% | 4.00% | 5.00% | |

| Capital requirements for equity security prospectus offerings post distribution are: | |||||||

| Post distribution capital requirements | 5520(2), 5521(2) and 5310(1) 10 | 25.00% | 50.00% | 60.00% | 80.00% | 100.00% | |

For all other offerings - The treatment of all other offerings is like that for equity security offerings with reductions in margin rates permitted where disaster out and/or market out clauses are in effect or where a Standard Form New Issue Letter has been obtained. Offerings, other than equity security prospectus offerings, are not eligible for the "normal new issue margin" rate reduction set out in IDPC Rule subsection 5130(5).

The following are suggested steps to be followed in determining the capital required for a particular underwriting.

Of note, a bought deal underwriting with a market out clause is not synonymous to an agency deal underwriting. IDPC Rule sections 5520 through 5522 recognize this distinction by requiring that either 5% or 10% of normal new issue margin be provided for the residual bought deal risk:

| Condition(s) met | Capital requirements for equity security prospectus offerings |

|---|---|

| No out clauses in effect | 100% of “normal new issue margin” |

| Disaster out clause in effect | 50% of “normal new issue margin” |

| New issue loan obtained | 10% of “normal new issue margin” |

| Disaster out clause in effect and new issue loan obtained | 10% of “normal new issue margin” |

| Market out clause in effect | 10% of “normal new issue margin” |

| Market out clause in effect and new issue loan obtained | 5% of “normal new issue margin” |

For all offerings, including fixed income security offerings, determine whether a capital requirement reduction, based on exempt purchaser expressions of interest, is available. For a Dealer Member to reduce its underwriting capital requirement, based on “expressions of interest” from exempt purchasers:

Where a Dealer Member takes advantage of this capital requirement reduction it should be noted that the reduction may be subject to an underwriting concentration charge, calculated pursuant to IDPC Form 1, Schedule 2A.

The existence of documented exempt purchaser11,12 expressions of interest will not result in any regulatory financial reporting accounting entries. Rather, the sole purpose for documenting exempt purchaser expressions of interest is to demonstrate that the syndicate manager has fully sold (but not yet contracted) the exempt purchaser allotment of a particular prospectus offering in advance of final prospectus clearance.

Where expressions of interest have been received for the entire exempt purchaser allotment, the syndicate group manager must inform the other syndicate group members on a timely basis that this has occurred13. Once provided with this information, the syndicate group members may provide a reduced capital amount on the exempt purchaser allotment portion of its underwriting commitment, in accordance with the conditions set out in IDPC Rule:

In the case of the syndicate group manager, the reduced capital amount on the exempt purchaser allotment portion of their underwriting commitment would not be available to them where the other members of the syndicate group have not yet been informed that the entire exempt purchaser allotment has been fully sold14.

The best approach to determining whether a syndicate group member can reduce its underwriting commitment and unsold security position, due to entering into sales arrangements with selling group or other dealers, is to determine whether the arrangement constitutes a committed or agency arrangement. In the event of a committed arrangement, the syndicate participant dealer may record a sale and the selling group dealer must record a commitment to purchase. In the event of an agency arrangement, the syndicate participant dealer may not record a sale. In the event the nature of the arrangement is not clear, the syndicate participant dealer may not record a sale.

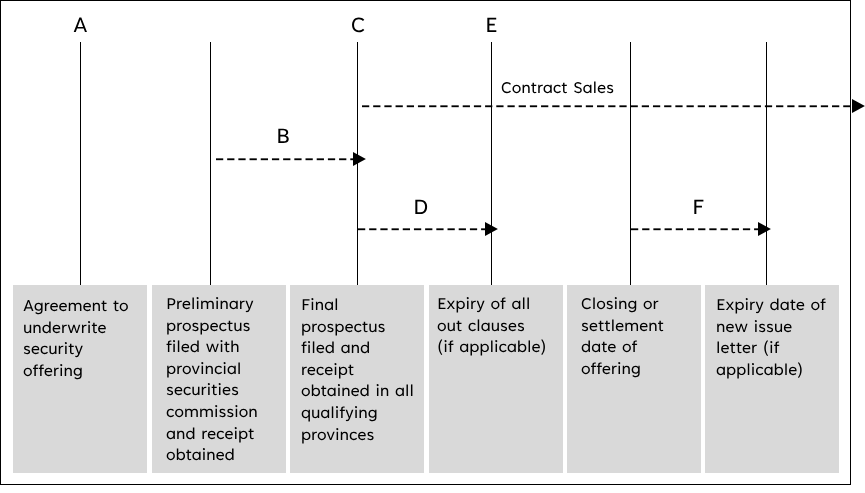

The image below summarizes the basic steps that take place in a prospectus offering. The commentary that follows the image details the approach to be followed in recording client sales of prospectus offering securities.

| A | Agreement date - The agreement date for an underwriting is the date the Dealer Member agrees (either verbally or in writing) with an issuer to underwrite a security offering. Whether or not this results in an underwriting commitment that needs to be recognized in the Dealer Member’s books as an obligation to the issuer is dependent upon the type of underwriting undertaken. In the case of an agency offering, the dealer is never committed to purchase the offering but has instead agreed to make best efforts to sell the offering to the investing public. As a result, no obligation to the issuer is recognized in the Dealer Member’s books. In the case of a committed offering, the dealer has agreed to purchase the offering from the issuer and has agreed to, among other things, the issue price, the size of share issuance and the total amount of the commitment. As a result, for a committed offering, the agreement date is considered to be the commitment date. It is on commitment date that the Dealer Member must record both its obligation to the issuer as a liability and the offering securities position it has agreed to buy as an asset. |

| B | Waiting period - In Ontario (OSA Section 65), the waiting period must be a minimum of ten days (five days for a POP issuer) between the issuance of the receipt for the preliminary prospectus and the issuance of the receipt for the final prospectus. During this period expressions of interest may be received from prospective purchasers. |

| C | Issuance date of Final Prospectus Receipt - As stated above, only expressions of interest may be received from prospective purchasers during the waiting period. As a result, the contracting of sales may not commence until the final prospectus receipt has been obtained. Current practice is to only permit the recording of public offering client sales when contracting takes place. |

| D | Expiry of out clauses - The close date is used as the reference date for the expiry of most out clauses. |

| E | All Out Clauses Expired |

| F | Expiry of New Issue Letter (also referred to as a “bank letter”). |

As discussed in Note C above, for a prospectus offering, the current practice is that client sales may be recorded when they are contracted and that sales may only be contracted after the receipt for the final prospectus is issued. This practice is followed, because it is considered unlikely that clients will exercise their right of withdrawal (found in OSA Section 71(2)) to any material degree.

This practice also applies to sales to exempt purchasers that are contracted by the syndicate manager on behalf of all the syndicate group members. Consistent with the guidance for documented exempt purchaser expressions of interest, the syndicate manager must inform the other syndicate group members on a timely basis when exempt purchaser sales are being contracted, to ensure all syndicate members are able to record their portion of the exempt purchaser sales (and reduce their unsold portion of the underwriting commitment) at the same time as the syndicate manager.

As regulatory approval of a private placement is not required, the approach to be followed in recording client sales of a private placement will differ amongst dealers and will differ somewhat from a prospectus offering. Current Dealer Member practices for recognizing private placement sales to clients differ. Dealer Members generally use one of three recognition approaches: (1) record a sale once a verbal trade to an accredited investor has been documented, (2) record a sale once a signed subscription receipt has been received from an accredited investor, or (3) record a sale once the dealer has contracted the sale to the accredited investor. Most dealers use either the first or second approach listed above.

CIRO staff are of the view that private placement sales can be recorded on the date a verbal commitment is received from an accredited investor, provided sufficient documentation of this verbal commitment is obtained and retained and there is no significant impairment in the market value of the private placement (in comparison to the issue price). For the purposes of applying this approach, CIRO staff expect that:

obtaining and retaining “sufficient documentation” would involve obtaining and retaining:

and

The table below compares the approaches to be followed in recording client expressions of interest and sales for prospectus offerings and client sales for private placement offerings:

| Prospectus offering | Private placement sales | ||

|---|---|---|---|

| Expressions of Interest | Sales | ||

| Exempt purchasers (defined as an “institutional” accredited investor but includes individual accredited investors that qualify as “institutional clients”16) | Expressions of interest are eligible for up to an 80% capital requirement reduction when:

[IDPC Rule section 5522] | Sales may be recorded when:

| Sales may be recorded when a documented verbal commitment is received from the exempt purchaser. |

| Retail accredited investor | Individual client renege rate unacceptable so no capital requirement reduction for documented expressions of interest [IDPC Rule section 5522 does not apply to retail accredited investors] | Sales may be recorded when:

| Sales may be recorded when:

|

| Other retail investors | Individual client renege rate unacceptable so no capital requirement reduction for documented expressions of interest [IDPC Rule section 5522 does not apply to other retail investors] | Sales may be recorded when:

| N/A – Private placements cannot be offered to clients that do not qualify as accredited investors |

IDPC Rule sections 5520 through 5522 stipulate that reduced capital may be provided on any unsold portion of the underwriting where out clauses (i.e. “market out” and “disaster out”) are in effect. Having said that, the risk reduction properties of these out clauses are only relevant in the event the Dealer Member exercises them. Where a Dealer Member provides reduced capital on an underwriting commitment due to an out clause being in effect, it is an indication that the Dealer Member assumes that the underwriting deal won’t proceed. Under these circumstances, it would be inappropriate for the Dealer Member to also record the underwriting fees that would be earned only if the underwriting proceeded.

In summary, underwriting fee revenue may be recorded when all underwriting agreement out clauses have expired or when a determination has been made by the Dealer Member that they will not be providing reduced capital on their underwriting commitment due to the presence of in effect out clauses. Where the out clauses contained in the Underwriting Agreement have not yet expired, the Dealer Member may choose to either:

As a practical matter, underwriting fee revenue will generally be recorded at or near the close date of the underwriting.

The current IDPC Rules do not prescribe precisely when the accounts maintained by the syndicate group manager for the underwriting revenues and expenses must be settled-up with the syndicate group members17. Nevertheless, consistent with the requirement for the syndicate group manager to inform all syndicate group members that the entire exempt purchaser allotment has been fully sold18, we expect the syndicate group manager to settle-up the syndicate accounts with all syndicate group members either on or within a reasonable period after the close date of the underwriting commitment.

Welcome to CIRO.ca!

You can find the Canadian Investment Regulatory Organization (CIRO) at CIRO.ca with our fresh look and feel.