A Powerful Force in Finance

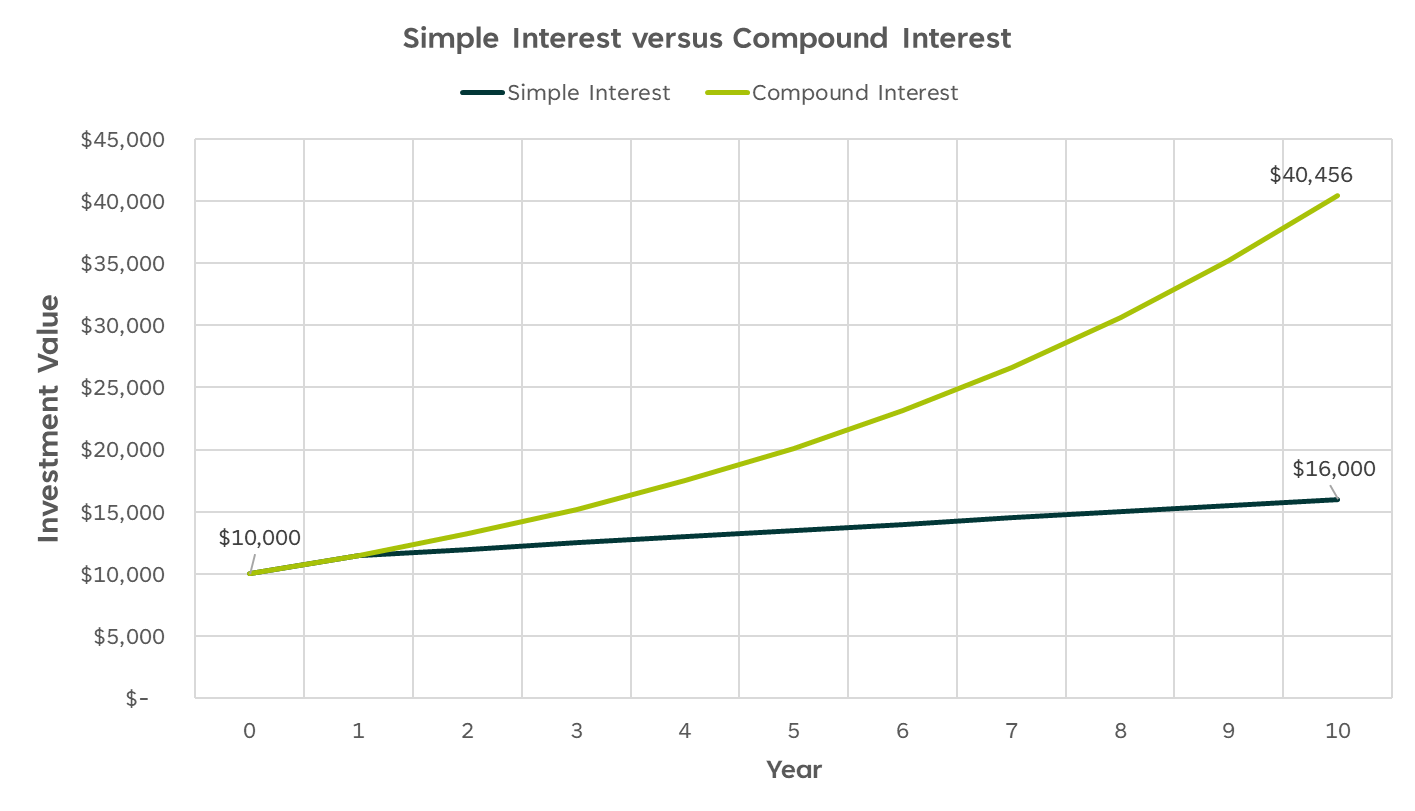

Compound interest, also known as compounding, is a financial concept that can turn small investments into large sums over time. Unlike simple interest, which is calculated only on the first amount of money invested, compound interest takes into account both the principal (first deposit) and the collected interest; you basically get to earn interest on interest.

When you continue reinvesting the interest that you earn on your deposits over a long period of time, you can speed up your growth.

Let’s break down compound interest using a simple example. Imagine you invest $1,000 at an annual interest rate of 5%. In the first year, you earn $50 in interest (5% of $1,000). Now, your total becomes $1,050.

Here’s where the magic of compound interest comes into play. In the second year, the interest is calculated not just on your initial $1,000 but on the new total of $1,050. So, at the same 5% interest rate, you now earn $52.50 in interest. Your total is now $1,102.50.

The greater the number of compounding periods, the greater the compound interest will be. Let’s take a look at another example to understand how compound interest is calculated.

Suppose you invest $1,000 at an annual interest rate of 5%, compounded annually. If you leave it untouched for 5 years and reinvest the interest, you’ll find that the future value is approximately $1,276.28. That’s a total of $276.28 in interest earned.

While you can calculate compound interest manually using the compound interest formula, it is recommended that you use a compound interest formula calculator. This way, you can ensure that the result is accurate and free from error. Check out the OSC’s Compound Interest Calculator.

FUN TIP

The Rule of 72 is another way to estimate compound interest. If you divide 72 by your rate of return, you will get a rough estimate of how long it’ll take for your money to double in value. For example, if you have $100 that was earning a 3% return, it would grow to $200 in 24 years (72 / 3 = 24).

Compounding is not limited to investments; it also applies to loans, where it works against you. Compound interest on borrowings or on debt can be very dangerous. When left unchecked, your debt can quickly spiral out of control, leaving you in financial ruin.

Understanding compound interest is crucial for making informed financial decisions, whether you’re saving for the future or managing debt. The key takeaway is that as an investor, time can be your friend when it comes to compound interest, so the earlier you start, the more your money can grow.

Key Features of Compound Interest:

Growth:

- Compound interest results in growth, where your money earns interest on both the initial investment and the previously earned interest. This compounding effect speeds up over time, leading to larger growth.

Principal and Interest:

- Unlike simple interest, which only considers the initial amount invested, compound interest combines both the principal and the accumulated interest. This combination increases the overall returns on your investment.

Frequency of Compounding:

- Common compounding frequency include annually, semi-annually, quarterly, or monthly. The more frequent the compounding, the faster your investment grows.

Time:

- Time is a powerful factor in compound interest. The longer your money is invested or borrowed, the greater the impact of compounding. Starting early can boost the final value of your investment.

Investment and Loan Applications:

- Compound interest is applicable to both investments and loans. When investing, it works in your favor, helping your money grow. However, with loans, it increases the total amount paid back over time.

Financial Planning Tool:

- Compound interest is a useful tool for financial planning. It assists individuals to estimate future returns on investments or understand the long-term cost of loans. This is important for making sound financial decisions.

Risk and Returns:

- While compound interest can lead to substantial returns, it’s essential to consider associated risks. Investments inherently involve some level of risk, and understanding the balance between risk and potential returns is vital for a well-rounded financial strategy.